Author: Andrei Dörre

Affiliation: Freie Universität Berlin, Institute of Geographical Sciences, Malteserstr. 74-100, 12249 Berlin, Germany

Email: andrei.doerre@fu-berlin.de

Language: English

Issue: 1/2025 (24)

Pages: 106–118 (13 pages)

Keywords: Special Economic Zones (SEZs), Free Economic Zones (FEZs), Tajikistan, economic policy, regional development, investment incentives, post-Soviet transition, infrastructure, Central Asia; global value chains, development planning

Abstract

Special Economic Zones (SEZs) have gained international prominence as instruments of economic policy intended to attract investment, stimulate industrial development, and reduce regional disparities. This article examines the implementation and performance of SEZs in Tajikistan—a low-income, post-Soviet economy marked by structural fragility, high labour migration, and pronounced regional inequalities. Drawing on two case studies, the Sughd and Ishkoshim Free Economic Zones (FEZ), the article demonstrates that while SEZs hold theoretical promise, their practical outcomes are highly contingent on infrastructural quality, geopolitical stability, and broader macroeconomic conditions. The Sughd FEZ has achieved modest success due to favourable location and infrastructure, whereas Ishkoshim FEZ illustrates the limits of overambitious planning in the absence of basic investment conditions. Overall, the contribution of SEZs to Tajikistan’s industrial output remains negligible, and the policy objective of mitigating regional disparities remains unmet. These findings underscore the importance of contextualised policy design and caution against overreliance on SEZs as a one-size-fits-all development tool.

Dr. Andrei Dörre

Dr. Andrei Dörre is a human geographer specialising in societal transformation and human–environment relations, with a regional focus on High Asia and post-socialist Central Asia. He teaches at the Institute of Geographical Sciences, Freie Universität Berlin, where he offers courses in human geography, regional geographies, and empirical research methods. His research has examined pastoral practices in Kyrgyzstan, development and security dynamics in Afghanistan, and small-scale irrigation and food systems in the Pamirs of Tajikistan. His current work explores collaborative resource management and socio-economic development in marginalised mountain regions. Dr. Dörre is a co-coordinator of the Working Group on High Mountain Research within the German Society for Geography and serves as an associate editor for the journals Pastoralism: Research, Policy and Practice and the Central Asian Journal of Water Research.

Introduction

Special Economic Zones (SEZs) are designated areas within a country where specific, business-friendly regulations apply. As an instrument of economic policy, SEZs are intended to attract investment in technologically advanced, capital-intensive, and future-oriented ventures. Moreover, they aim to serve as growth poles for economic development, enhance a country’s integration into the globalized economy, and contribute to the reduction of regional disparities. This article introduces the concept and illustrates its implementation in Tajikistan through the example of two Free Economic Zones (FEZs).

The term Special Economic Zone has emerged internationally as a collective designation for “geographically delimited areas within which governments facilitate industrial activity through fiscal and regulatory incentives and infrastructure support.”[1] The regulatory frameworks of such zones typically include exemptions from customs duties and taxes, state subsidies, and legal deregulations. The use of exceptional regimes for income generation and economic stimulation is not a novel phenomenon. As early as the Hanseatic League, free ports, and overseas outposts of European powers reaped significant revenues through the provision of trade privileges.

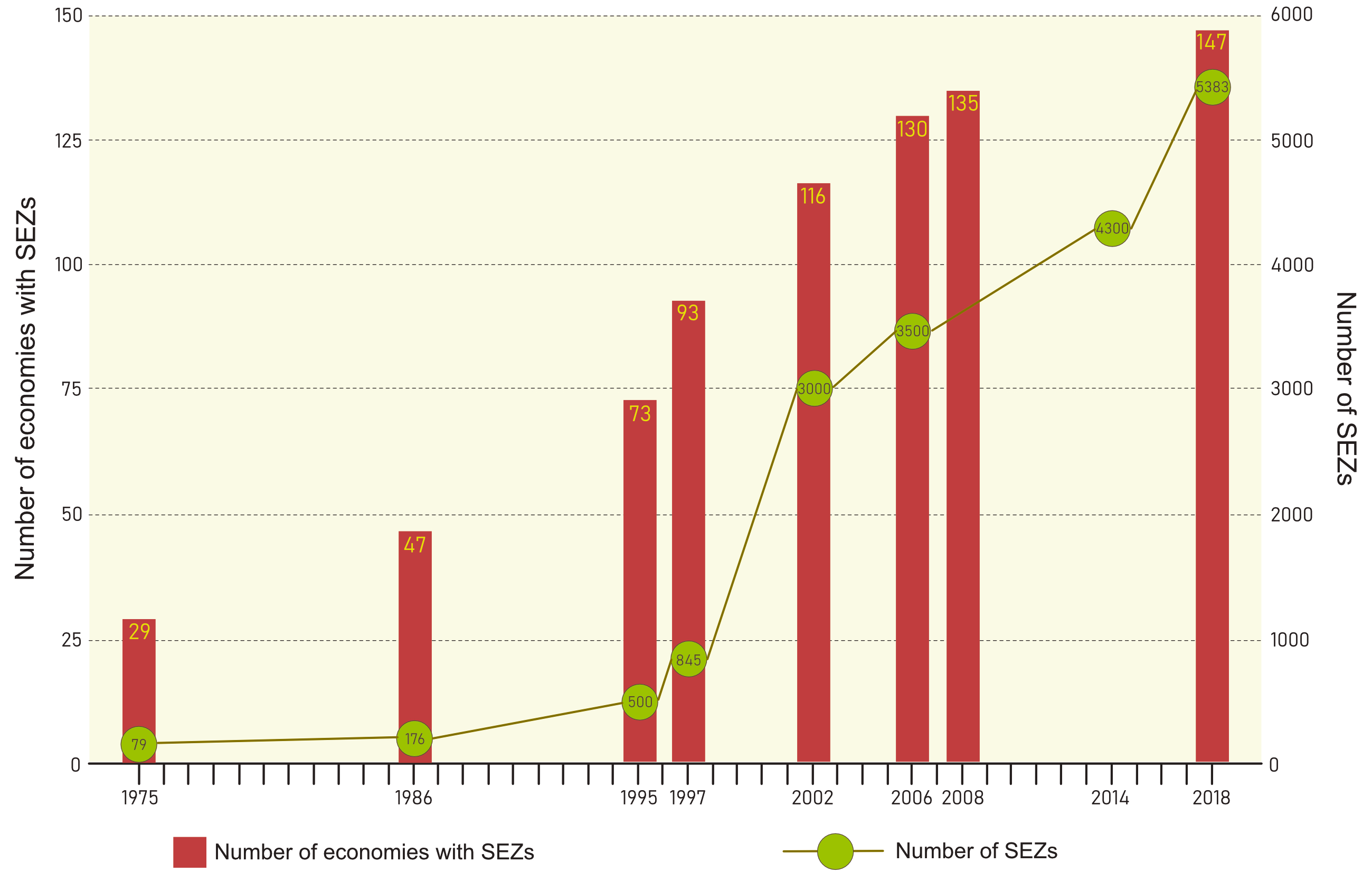

In the 20th century, the designation of Free Industrial Zones began to take shape—for instance, in 1959 at Shannon Airport in Ireland, formerly a hub for propeller-driven transatlantic flights. This initiative aimed to revitalize the regional economy in the new era of jet aviation. A diachronic perspective reveals that, with globalization—understood as the intensification of international exchange, mobility, and transnational networks of production, value creation, and supply chains—both the number of SEZs and the number of countries employing this policy instrument have risen steadily. By 2018, nearly 5,400 such zones had been identified across 147 countries, with China accounting for the largest share, operating over 2,500 (see Figure 1). Notable examples of SEZs worldwide include Qeshm Island (Iran) in the Persian Gulf, the Panama Pacifico Special Economic Area (PPSEA) in Panama, and the metropolis of Shenzhen in China.

Source: Author’s own design based on UNCTAD 2019, p. 129

Diverse Objectives

Low-income countries primarily pursue the development of export-oriented industries and infrastructure by offering business-friendly investment conditions. In doing so, they aim to integrate into global value chains and create employment opportunities. North Korea, with its currently closed Kaesong Industrial Zone, belongs to this category. Middle-income countries tend to focus on upgrading and diversifying existing industries, achieving deeper integration into international supply and value chains, promoting technology and innovation transfer, and facilitating the transition to a service-based economy. The Dominican Republic, which operated 73 SEZs as of 2019, exemplifies this group. High-income economies often employ SEZs to establish platforms for managing complex supply chains.[2] Japan, for instance, operates a logistics center with SEZ status on the island of Okinawa.

Across these categories, four core objectives can be discerned: 1) virtually all zones aim to attract capital; 2) they are designed to support the expansion of export sectors; 3) they serve as instruments for employment generation; and 4) they function as testing grounds for market-liberal policy programs prior to their broader implementation.

This approach has provoked criticism from various quarters. One concern is the accusation of export subsidization, which implies a violation of a fundamental principle of the World Trade Organization.[3] Further criticisms include the overemphasis on export orientation and the frequent absence of spillover effects beyond zone boundaries, the prevalence of precarious working conditions, and inadequate state oversight of local processes. The uncertain net effects of SEZs are also highlighted, particularly in light of domestic tax avoidance strategies observed in countries such as China.[4] Reduced environmental standards raise fears of pollution and public health risks—issues already documented in relation to Mexico’s tariff-free maquiladoras and SEZs in Sri Lanka.[5] Additionally, expropriations and the destruction of established livelihoods have been reported in connection with the establishment of SEZs lacking democratic legitimacy, as seen in the Indian state of Rajasthan.[6]

Special Economic Zones in Central Asia

With the dissolution of the Soviet Union in 1991, the newly independent Central Asian states lost the economic support previously provided by the former Soviet center. In an effort to stimulate autonomous economic development, a range of measures were adopted, including the establishment of SEZs in the early 2000s. This development must also be viewed in the context of China’s “Belt and Road Initiative,” as governments in this region—understood as a strategic bridge between China and Europe—anticipate investment from their economically ascendant neighbor (see Table 1). The following section presents two examples to illustrate how the SEZ policy instrument has been implemented in Tajikistan.

Table 1: Regional foreign direct investment in Central Asia in 2018 (in billion US$, rounded)

| Investor (column) / Recipient (row) | Afghanistan | China | Kazakhstan | Kyrgyzstan | Tajikistan | Turkmenistan | Uzbekistan | Total investments in the recipient country from the countries of the region |

|---|---|---|---|---|---|---|---|---|

| Afghanistan | 0.39 | – | – | – | – | – | 0.39 | |

| China | 0.005 | 0.06 | 0.01 | 0.001 | 0.001 | 0.002 | 0.08 | |

| Kazakhstan | – | 8.27 | 0.01 | 0.001 | – | 0.012 | 8.29 | |

| Kyrgyzstan | 0.002 | 1.35 | 0.18 | 0.002 | n/a | 0.002 | 1.53 | |

| Tajikistan | 0.002 | 1.44 | 0.05 | 0.002 | – | – | 1.49 | |

| Turkmenistan | – | 0.19 | – | – | – | – | 0.19 | |

| Uzbekistan | – | 0.85 | 0.07 | – | – | – | 0.92 | |

| Total investments of the investing country in the countries of the region | 0.009 | 12.49 | 0.36 | 0.02 | 0.004 | 0.001 | 0.016 |

Source: CAREC 2021, p. 14

Special Economic Zones in Tajikistan

Tajikistan is a low-income economy, the smallest in Central Asia, and is characterized by pronounced regional disparities, limited industrial diversification, and a weak secondary sector. It exhibits one of the highest labor migration rates globally and remains heavily dependent on remittances sent home by migrant workers.[7] Against this backdrop, a law on “Free Economic Zones” was introduced in 2004 and replaced by the current legal framework in 2011. According to this law, Free Economic Zones (FEZ) are defined as areas governed by preferential legal provisions to facilitate business and investment activities.[8] The primary objectives include the development of regional economic potential, the promotion of export-oriented and import-substituting industries, the establishment of modern production facilities and technologies, and the creation of employment opportunities.[9] To date, five FEZs have been designated. Four are located in the economically stronger Western and Northern regions of the country, while one is situated in the East (see Figure 2).

Design: A. Dörre 2025

Data available since 2017/2018 shed light on the outcomes achieved thus far. Overall, the results are underwhelming in terms of the number of operating enterprises, job creation, foreign direct investment, and production volumes. While the Sughd and Dangara FEZs exhibit signs of emerging economic dynamism, the outcomes in the Panj and Ishkoshim FEzs appear stagnated. The absence or low levels of activity in the Kulob FEZ can be attributed to its recent establishment in March 2019 (see Table 2).

Table 2: Selected key indicators of FEZs in Tajikistan

| Registered Enterprises (Industry/Services) |

Employment | Direct Investment in Million Tajik Somoni (TJS) |

Production Output in Million Tajik Somoni (TJS)*** |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FEZ/year | 2018 | 2019 | 2020* | 2018 | 2019 | 2020 | Before 2017 | 2017 | 2018 | 2019 | 2020 | Before 2017 | 2017 | 2018 | 2019 | 2020 |

| Sughd | 24 (20/4) | 29 (24/5) | 30 (19/6/5) | 519 | 599 | 668 | n/a | 11,35 | 19,07 | 9,5 | 16,9 | 252,5 | 80,1 | 116,1 | 163,2 | 165,26 |

| Dangara | 27 (21/6) | 25 (22/3) | 22 (6/16/-)** | 456 | 407 | 350 | n/a | 91,09 | 36,8 | 129,2 | 24,3 | 20,9 | 19 | 25,3 | 36,8 | 34,5 |

| Kulob | 1 (1/-/-) | 19 | n/a | n/a | ||||||||||||

| Panj | 17 (13/4) | 16 (12/4) | 11 (4/3/4) | 49 | 52 | 35 | n/a | 6,2 | 3,38 | 3,9 | 2,1 | 0,37 | 0,25 | 0,29 | 0,8 | 0,5 |

| Ishkoshim | 3 (1/2) | 5 (4/1) | 5 (5/-/-) | 22 | 14 | 20 | 0 | 0 | 0,2 | 3,7 | 0 | 0 | 0 | 0,04 | 0,03 | n/a |

| Total | 71 (55/16) | 75 (62/13) | 69 (35/25/9) | 1046 | 1072 | 1092 | 1551.9 | 108.64 | 59.45 | 146.3 | 43.3 | 273.8 | 99.4 | 141.7 | 200.83 | 200.26 |

| * For 2020, the ministry does not provide a sectoral breakdown, but a differentiation according to the origin of the established companies (domestic/foreign/mixed participation). ** The ministry provides different figures for Dangara FEZ. For this overview, the most detailed figures have been used. *** The total volume of services and cross-border trade is said to have amounted to around 25 million TJS since the beginning of the FEZs. |

||||||||||||||||

Source: MEDTRT 2021, own calculations

Modest Successes in Sugd

Established in 2008, the Sughd Special Economic Zone is located in the eponymous and economically most advanced province of Tajikistan, in close proximity to the major city of Khujand, several border crossings with Uzbekistan and Kyrgyzstan, as well as key infrastructure such as cross-border road networks, railway lines, and an international airport (see Figure 2). The regulatory framework for this 320-hectare zone reiterates the goals and functions outlined in national legislation and defines light and biochemical industries, construction materials, mechanical and domestic engineering, and services as its core sectors.[10] Incentives include extremely low rental and lease rates: US$ 5/m² per month for enclosed warehouses, US$ 3/m² per year for production and office spaces, and as little as US$ 1/m² per year for open areas. Further benefits include full exemption from customs duties and partial tax relief. Foreign investors and employees are offered support in obtaining visas. Strikes are prohibited.[11]

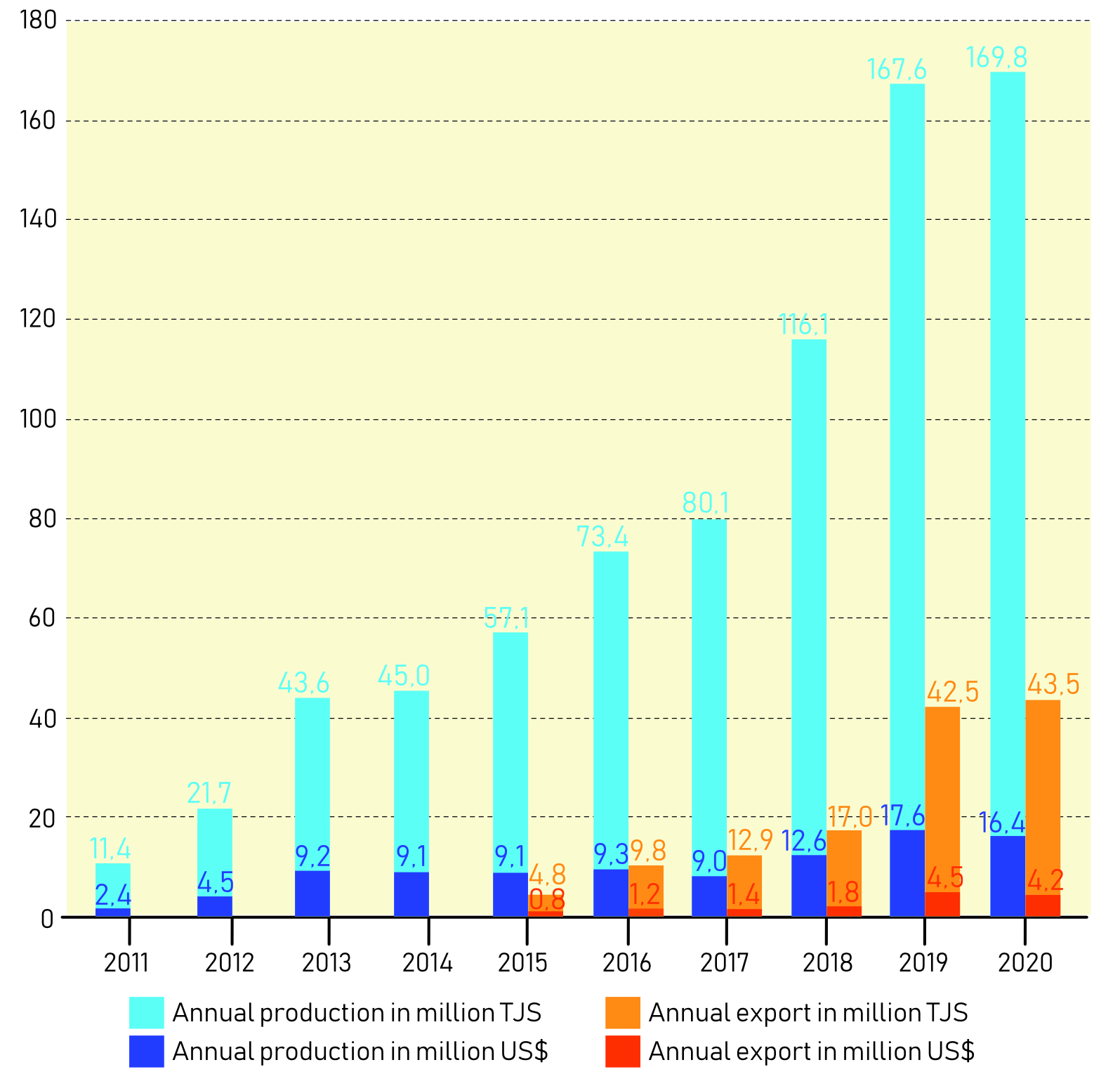

To date, the zone’s performance can be described as a modest success. Thirty enterprises have been established, twelve of which involve foreign participation. By 2021, Turkey leads with four ventures, followed by China with two, and Kazakhstan, Cyprus, Poland, Uzbekistan, Canada, and Kuwait each with one.[12] Total investment amounts to approximately 97 million Tajik Somoni (TJS), significantly below the projected 244.5 million TJS. The workforce comprises around 670 employees, 90% of whom are local, and who earn an average monthly wage of 1,200–1,500 TJS—well above the national average. However, this figure also falls short of the targeted 1,200 jobs. In terms of production—particularly of construction materials, furniture, children’s toys, and dried fruit, primarily for the domestic market—the zone has demonstrated steady growth when measured in TJS. In 2020, it accounted for approximately 11% of the annual industrial output of the city of Khujand, and 1% of that of the Sughd province. Since 2015, exports of these goods have been confined to Central Asia and have also shown continuous growth.[13] Yet when both production and exports are measured in US$, the standard currency for international trade, the picture changes considerably, primarily due to the declining exchange rate of the national currency (see Figure 3).

Source: Author’s own design based on AFEZ-S 2021a

At present, the zone does not host any innovative or forward-looking technological enterprises.[14]

Stagnation in Ishkoshim

Established in 2011, the Ishkoshim FEZ spans 200 hectares and is located in the Autonomous Province of Gorno-Badakhshan, in the easternmost part of Tajikistan, directly bordering Afghanistan. The site was chosen at the initiative of local entrepreneurs who aimed to establish a commercially viable trade and production hub in what was perceived to be a strategically advantageous location. The objectives included cost-efficient trade in regional goods, revitalization of the peripheral high mountain economy, and the diversification of local income opportunities. The zone’s purported advantages include direct access to the road network of Afghanistan, a nearby Soviet-era airfield, and the proposed road connection to the “China–Pakistan Economic Corridor” via the Dorah Pass at the border between Afghanistan and Pakistan, the yet-to-be-opened Tajik-Afghan border post at Langar Kikhn, and the Wakhjir Pass linking Afghanistan and China.[15]

The goals, incentives, and sectoral priorities outlined in the regulatory framework largely mirror those of the Sughd zone. Emphasis is placed on the processing of agricultural produce, regionally sourced wool fibers, animal hides, and natural stone, as well as tourism and health-related services.[16] These priorities align well with local conditions, including a nearby mine producing spinel (a gemstone used in jewelry), livestock farming, and a number of thermal springs considered suitable for health tourism.

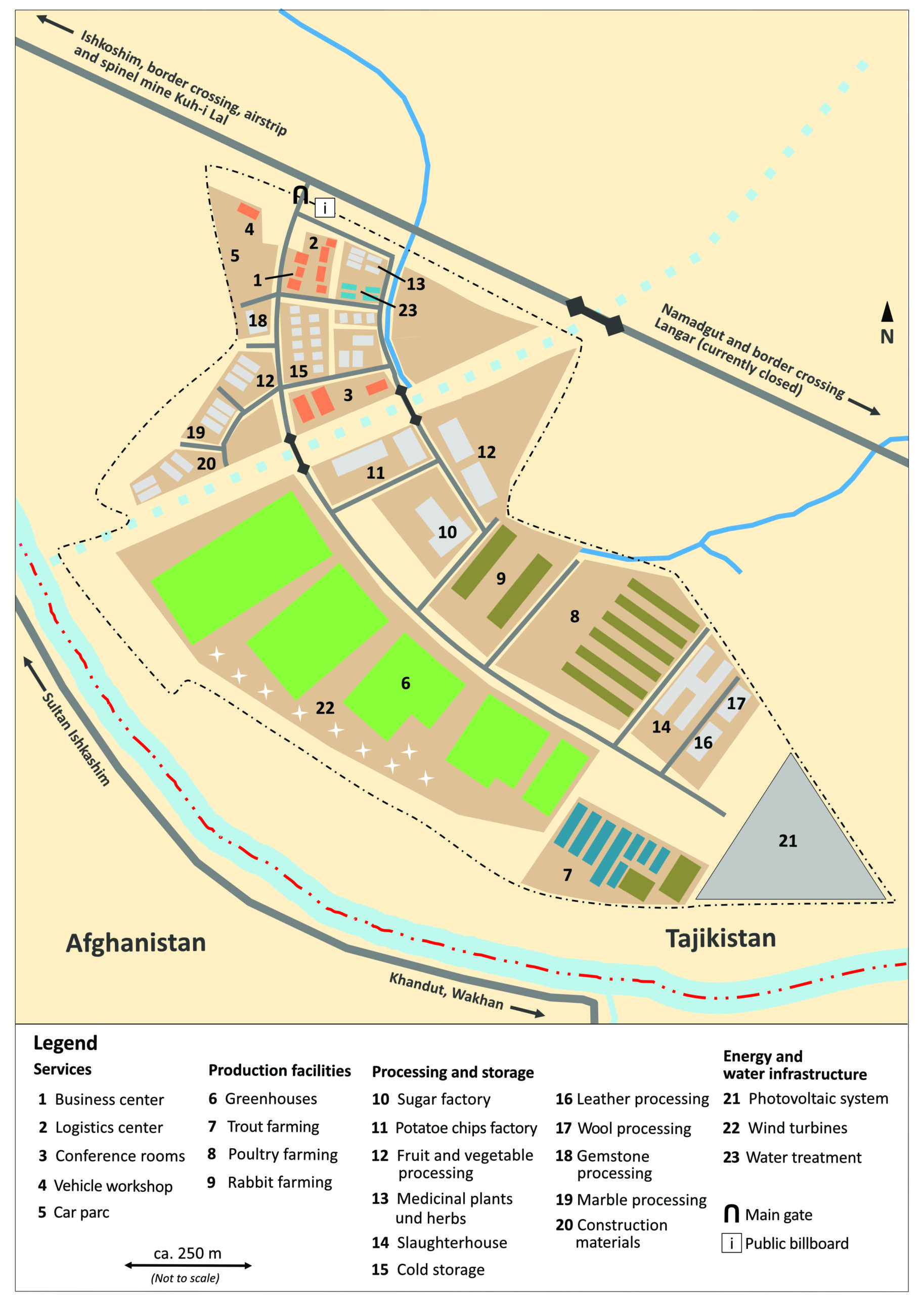

However, what most characterizes this FEZ—described locally as a crossroads of four nations—is less the actual economic output than its ambitious vision and the detailed conceptualization of its perceived development potential. A publicly displayed land-use concept outlines planned facilities for agricultural production, animal husbandry and processing, light and construction industries, gemstone refining, and even renewable energy generation (see Figure 4, and Figure 5).

Photograph: Dörre 2018

Design: Dörre 2025 based on the Public billboard (Figure 4)

A closer look behind the perimeter fence, however, reveals stagnation. Only a handful of local entrepreneurs have registered operations. Production, job creation, and cross-border trade remain minimal. In its current state, the Ishkoshim FEZ represents a “white elephant”—a failed investment project (see Table 2; Figure 6). According to various sources, the unsatisfactory performance can be attributed to four primary factors: 1) Instability in Afghanistan, which renders substantial cross-border movement of goods and people, as well as stable cooperation and exchange relationships, unfeasible. 2) High transport costs persist due to poor road conditions and the lack of renovation and reactivation of the airstrip, hampering the swift movement of inputs, products, and people. 3) The absence of basic infrastructure, such as water supply, electricity, and internet connectivity, deters potential investors. These deficiencies require significant additional investment in what should be basic provisions supplied by the FEZ administration, leading to project delays. 4) A shortage of qualified personnel and the overall lack of appeal of Ishkoshim as a place to live further diminish its attractiveness to investors.[17]

Photograph: Dörre 2018

Conclusion

The examples presented illustrate that while SEZs in the context of Tajikistan may initially appear to be promising policy instruments, their implementation does not necessarily guarantee success. Incentives alone are insufficient to persuade potential investors if regional and local conditions render engagement too risky or unprofitable. The performance of SEZs appears to be closely linked to the strength and competitiveness of the host economy. This helps explain why, unlike in Kazakhstan—a middle-income country—major foreign investments have thus far bypassed Tajikistan’s SEZs. In 2020, FEZs contributed less than 1% to Tajikistan’s industrial output, offering little in the way of momentum for broader economic growth. The objective of reducing regional disparities through such zones thus remains a distant goal. At the local level, however, a more nuanced picture emerges. The Sughd FEZ, benefitting from robust infrastructure, a location within the country’s most economically dynamic region, and integration into the urban economy of Khujand, possesses locational advantages that have enabled modest success. In contrast, in Ishkoshim, overly ambitious concepts and aspirational planning collide with investment-deterring realities. Taken as a whole, it must be concluded that outcomes to date have fallen short of expectations.

[1] UNCTAD 2019, p. 128

[2] UNCTAD 2019, pp. 141, 148

[3] Moberg 2015, pp. 170–171

[4] Kerkow and Martens 2010, pp. 12–20

[5] FIAS 2008, p. 41

[6] Levien 2011

[7] CIA 2021

[8] RoT 2011, Art. 1

[9] RoT 2011, Art. 3

[10] RoT 2008, Arts. 1, 3

[11][11] RoT 2008, Arts. 8–12

[12] AFEZ-S 2021a; AFEZ-S 2021b

[13] AFEZ-S 2021a

[14] AFEZ-S 2021a

[15] AFEZ-I 2020; Barratt 2016, p. 17; Levi-Sanchez 2017, p. 101

[16] RoT 2010, Arts. 1, 3, 8–12

[17] AFEZ-I 2020; Barratt 2016, p. 17; Khurramov 2020

References

AFEZ-I. Administration of the Free Economic Zone “Ishkoshim”. 2020. Consultation with the management of the FEZ.

AFEZ-S. Administration of the Free Economic Zone “Sughd”. 2021a. Shortly about Sughd Free Economic Zone (unpublished material). Khujand.

AFEZ-S. Administration of the Free Economic Zone “Sughd”. 2021b. Subjects. Available: http://fezsughd.tj/en/subjects/

BARRATT, Stefanie. Assessment of Economic Opportunities Along the Afghan–Tajik Border. Dushanbe: 2016.

CAREC – Central Asia Regional Economic Cooperation Institute. CAREC Regional Integration Index (CRII). Urumqi: 2021.

CIA – Central Intelligence Agency. The World Fact Book. Countries: Tajikistan. Available: https://www.cia.gov/the-world-factbook/countries/tajikistan/

FIAS – Foreign Investment Advisory Service. Special Economic Zones: Performance, Lessons Learned, and Implications for Zone Development. Washington, DC: 2008.

KERKOW, Uwe; MARTENS, Jens. Sonderwirtschaftszonen. Entwicklungsmotoren oder teure Auslaufmodelle der Globalisierung? Düsseldorf, Bonn, Osnabrück: 2010.

KHURRAMOV, Khursand. Nesvobodnaya Ekonomicheskaya Zona? Kak Izmenilas’ SEZ “Ishkashim“ za poslednie 10 let. 2020. Available: https://rus.ozodi.org/a/30912623.html

LEVIEN, Michael. Special Economic Zones and Accumulation by Dispossession in India. Journal of Agrarian Change, 2011, vol. 11, no. 4, pp. 454–483. https://doi.org/10.1111/j.1471-0366.2011.00329.x

LEVI-SANCHEZ, Suzanne. The Afghan–Central Asia Borderland. The State and Local Leaders. London: Routledge, 2017. https://doi.org/10.4324/9781315691718

MEDTRT – Ministry of Economic Development and Trade of the Republic of Tajikistan. Activities of the Free Economic Zones of the Republic of Tajikistan 2019–2021. Available: http://fez.tj/

MOBERG, Lotta. The Political Economy of Special Economic Zones. Journal of Institutional Economics, 2015, vol. 11, no. 1, pp. 167–190. https://doi.org/10.1017/S1744137414000241

RoT – Republic of Tajikistan. Law of the Republic of Tajikistan “On Free Economic Zones”. 2011. Available: https://www.wto.org/english/thewto_e/acc_e/tjk_e/wtacctjk23a1_leg_2.pdf

RoT – Republic of Tajikistan. Regulation of Free Economic Zone “Ishkoshim”. 2010. Available: http://tpp.tj/business-guide2017/pdf/pdf_eng/fez/01%20-%20Regulation%20of%20FEZ%20ISHKOSHIM.pdf

RoT – Republic of Tajikistan. Regulation of Free Economic Zone “Sughd”. 2008. Available: http://fezsughd.tj/en/legal-framework/

UNCTAD – United Nations Conference on Trade and Development. World Investment Report 2019. Special Economic Zones. New York, Geneva: 2019.